Corporations like to complain that their federal income tax rates

are too high. But lost amid the clamor to cut taxes for corporations is the fact that U.S. corporations are paying a

far lower share of our nation’s total tax revenues. In fact, many of the nation’s largest companies are paying little or no federal taxes at

all.

The top federal income tax rate for corporations, as for some individuals,

is 35 percent. But while the top income tax rate is the same for individuals and corporations, corporations have been

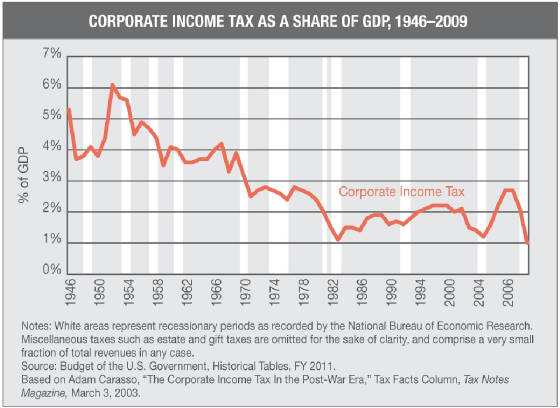

paying a lower share of our nation’s total taxes. Overall, the nation’s federal revenue from corporate income

tax receipts, as a percentage of the nation’s gross national product, dropped dramatically to one-sixth of that in the 1950s.[1]

As the corporate share of our nation’s federal tax revenue

has fallen, individual Americans have paid a relatively higher percentage of federal tax revenue. Corporate taxes fell from 26.4 percent

of total tax revenue in 1950 to just 7.4 percent of total tax revenue in 2010. During this same period, personal income, Social Security and Medicare taxes

increased from 51.4 percent to 83.8 percent of total tax revenue.[2]

Thanks to numerous tax breaks and loopholes, corporations rarely

pay the full corporate income tax rates. A 2011 report by Citizens for Tax Justice and the Institute on Taxation and Economic Policy found that 78 of 280 of the nation’s largest and most profitable companies paid no federal income taxes

in at least one of three years.[3]

Overall, the study found that the Fortune 500 companies included in the survey paid 18.5 percent in taxes, or about half the

corporate income tax rate of 35 percent.[4]

Perhaps even more startling, many of the largest companies are now

paying less tax than before the Wall Street financial crisis and economic recession, even though their profits have recovered.

Cash tax payments by non-financial companies in the S&P 500 index fell 13.2 percent to $222 billion in 2010 from 2007,

according to Bloomberg data, while net income rose 12.5 percent to $612 billion.[5]

How do they do it? One tax avoidance strategy that many companies

use to enrich their top executives is to pay hefty amounts of stock options. The tax code allows companies to deduct

the appreciated value of stock options when their executives exercise them, instead of the lower value of the stock options

at the time they were granted.[6]

For years, Sen. Carl Levin (D-Mich.) has been pushing for legislation

that would limit the tax deductions companies could claim on stock options.[7] The bipartisan Joint Committee on Taxation

has estimated that if the Levin bill were enacted it would add $25 billion in revenue to the federal government over the next

decade. [8]

Another corporate tax avoidance strategy is to move overseas to an offshore

tax haven like Bermuda. By reincorporating offshore, companies avoid paying federal income taxes on profits earned outside

the United States.[9] This strategy of registering in an offshore tax

haven is particularly attractive for hedge funds. Hedge Fund Research estimates that of the $1.86 trillion invested in hedge

funds, $1.25 trillion is kept offshore.[10]

[1] Office of Management and Budget, Budget of the US Government

FY 2011, Historical Tables, Table 2.3, available athttp://www.gpoaccess.gov/usbudget/fy11/sheets/hist02z3.xls.

[2] “Corporate Taxpayers & Tax Dodgers, 2008-2010,”

Citizens for Tax Justice and the Institute on Taxation and Economic Policy, November 3, 2011.

[3] Ibid.

[4] “Corporate Taxes Fail to Follow Profit Rebound to Pre-2008

Highs,” Bloomberg News, December 6, 2011.

[5] “Tax Benefit From Options As Windfall for Businesses,”

The New York Times, December 30, 2011.

[6] Ibid.

[7] Ibid.

[8] “Benefits of Incorporating Abroad in an Age of Globalization,”

Steven M. Davidoff, The New York Times, December 21, 2011.

[9] “How Average Taxpayers Subsidize Runaway Pay,” Executive

Excess 2008, Institute for Policy Studies, August 25, 2008.

[10] “Corporate Income Tax as a Share of GDP,

1946-2009,” Tax Policy Center, April 15, 2010, available athttp://www.taxpolicycenter.org/taxfacts/displayafact.cfm?Docid=263&Topic2id=70.